Crypto Business: Fragmented Investment Strategies and the Absence of Capital Consensus

As of May 2026, the digital asset market is dividing into fragmented investment themes. With Bitcoin dominance, the rise of Ethereum, the mining industry's shift to AI, and capital inflows into tokenized Treasuries coexisting, the unified bull narrative of the past has lost its momentum.

As of May 2, 2026, the digital asset market has entered a phase of severe fragmentation where the unified 'crypto' narrative of the past has dissolved, and disconnected investment logics coexist. While venture capital allocation reached multi-year highs at the end of 2025, the current landscape is defined by mining companies pivoting to artificial intelligence (AI), a tug-of-war over Bitcoin dominance, and institutions retreating into safe-haven assets like tokenized Treasuries.

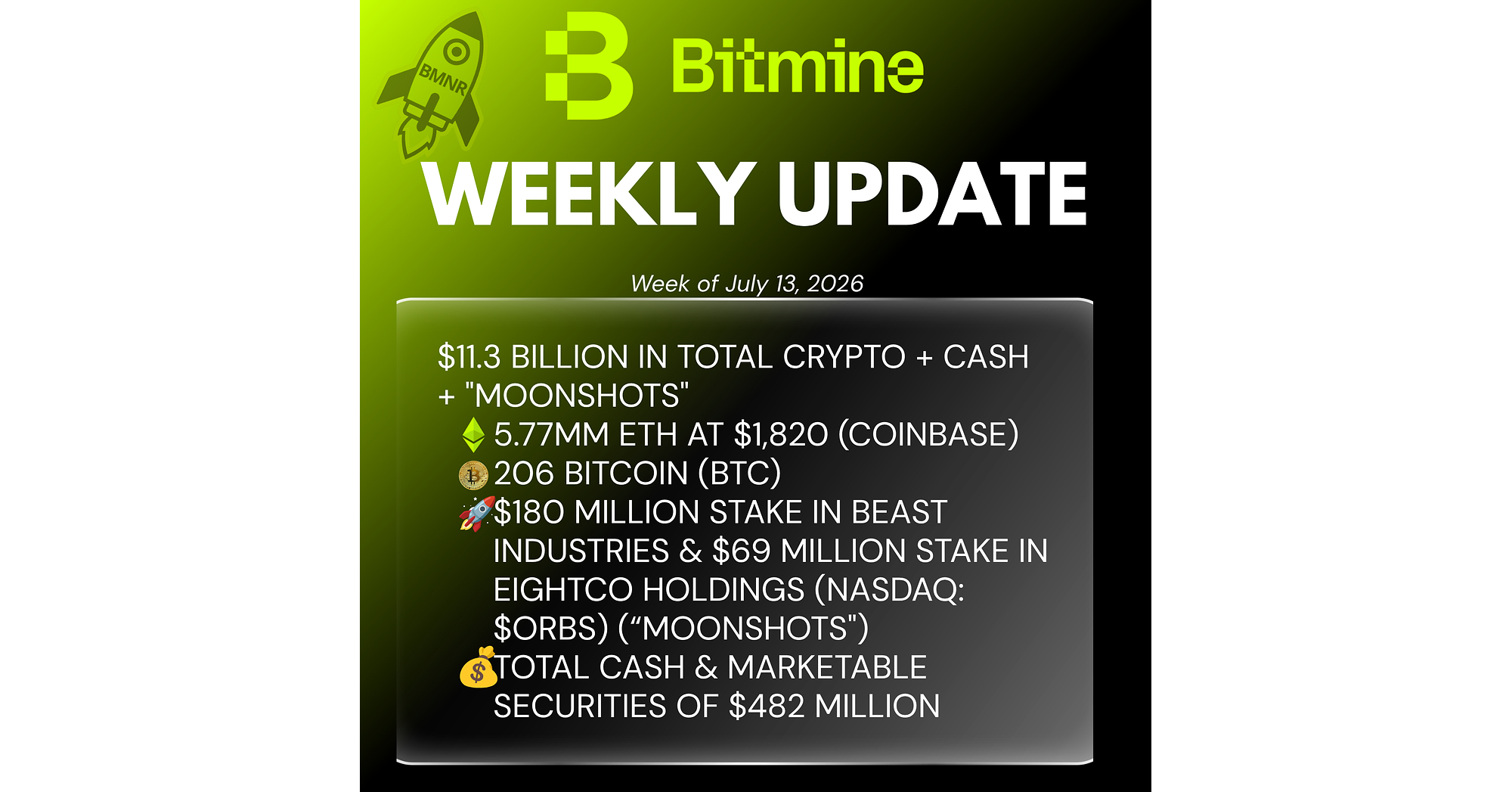

The crypto market is fracturing as miners pivot to AI, BitMine doubles down on Ethereum, stablecoin liquidity remains idle, and tokenized Treasuries reshape trading collateral.

The market's fragmentation is evident in specific industrial shifts. While major players like BitMine are doubling their investment in the Ethereum ecosystem, the traditional Bitcoin mining industry is seeking to diversify revenue by converting computational power into AI infrastructure. At the same time, the phenomenon of stablecoin liquidity remaining idle within the market without finding immediate investment opportunities suggests that capital is taking an extremely cautious stance.

Venture Capital's Disciplined Rebound and Fundamental-Driven Restructuring

Throughout 2025, crypto venture capital investment recorded approximately $18.9 billion, a significant rebound from $13.8 billion in 2024. Notably, $8.5 billion was deployed in the fourth quarter of 2025 alone, the largest quarterly volume since Q2 2022. In contrast to the indiscriminate investment fever of the past, these capital inflows tend to concentrate on projects with revenue-generating capabilities and regulatory compliance.

- Securing actual revenue traction and unit economics

- Regulatory-compliant architecture including KYC and custody functions

- Token economic model design linked to cash flow

- Potential for convergence with AI and Decentralized Physical Infrastructure (DePIN)

Investors are now prioritizing fundamentals over mere FOMO (fear of missing out). As the 2021-style speculative cycle concludes, the market is being led by a small group of disciplined core investors. They are prioritizing funding for infrastructure and consumer applications that demonstrate high capital efficiency and a tangible user base.

The competition for institutional preference between Bitcoin and Ethereum is also intensifying. As of April 2026, Bitcoin's market dominance fluctuates between approximately 58.2% and 59.26%, still leading the overall market trend. In particular, $1.7 billion flowed into Bitcoin spot ETFs last January, proving strong institutional demand, but recently, the possibility of capital rotation into Ethereum has been cautiously raised, gaining traction for the outlook that this will be 'Ethereum's year.'

Industrial Transition: From Mining to AI and Tokenized Real-World Assets

Major asset managers, including Grayscale, are noting AI, DePIN, and Intellectual Property (IP) as macroeconomic catalysts for 2026. As mining companies expand their business models beyond simple cryptocurrency mining into data center infrastructure for AI computation, digital ownership models are maturing and creating new growth engines.

The tokenization of Real-World Assets (RWA) is also accelerating. Supported by large financial institutions like BlackRock and J.P. Morgan, tokenized Treasuries and real estate are serving as bridges between traditional finance and digital markets. This goes beyond simple asset digitalization, as they are being utilized as reliable collateral assets on-chain, fundamentally changing the market's liquidity structure.

Q1 2026 performance data shows extreme yield gaps between assets. During this period, while Bitcoin prices fell by 22.0%, showing weakness alongside the stock market, commodity prices such as West Texas Intermediate (WTI) surged by 76.9%, presenting a stark contrast. Additionally, a deleveraging phenomenon in algorithm-based assets was observed, such as Ethena's USDe supply shrinking to $5.9 billion.

Institutional trading activity remains robust. Looking at spot trading volume over the last seven days, Bitcoin recorded $354.4 billion, Ethereum $300.7 billion, and Solana $60.0 billion. This high trading volume is analyzed to have occurred not from simple selling, but from institutional accumulation and portfolio restructuring centered on regulation-ready assets.

In conclusion, the crypto market in 2026 is characterized by abundant capital but a lack of a single direction. Investors are now deploying funds based on specific sectors and revenue models rather than the umbrella term 'crypto.' The future direction of the market depends on when and into which themes idle stablecoin liquidity will flow, and whether Ethereum can substantially erode Bitcoin's dominance.

| Asset | 7D Spot Volume (Early 2026) | Q1 2026 Price Change |

|---|---|---|

| Bitcoin (BTC) | $354.4B | -22.0% |

| Ethereum (ETH) | $300.7B | N/A |

| Solana (SOL) | $60.0B | N/A |

Comparison of trading volumes and price performance for major assets in early 2026.

This content is for information and commentary only and is not investment advice.

Join the reader conversation

Read reactions to this article and leave your own note.